Why mortgage broker PPC can be a powerful – yet pricey – channel

mortgage broker PPC can deliver high-intent prospects fast, but it isn’t a set-and-forget channel. The clicks are expensive, conversion windows are long, and many leads start online and finish by phone or offline paperwork. If you want paid search to pay off, you need clear measurement, disciplined targeting, and a plan that values quality over volume.

What costs look like in the real world

In most markets, keyword competition for mortgage queries means cost-per-clicks in the tens of dollars. Top commercial queries are usually higher. That reality shapes the whole funnel: expensive CPCs plus low conversion rates demand a relentless focus on lead quality. For many brokers, the math depends on three numbers: cost per lead, close rate, and lifetime value. Push any one of those in the right direction and the program becomes viable. See Google Ads industry benchmarks for context: Google Ads industry benchmarks.

Typical operational ranges seen in 2024 – 2025 put cost-per-lead between roughly $50 and $400. Why such a wide band? It comes down to how you target keywords, how you qualify visitors, and whether you capture offline conversions properly. You can run mortgage broker PPC on a tight local budget and get $60 leads, or bid broadly and pay $300 for the same-sounding query elsewhere. See broader PPC context in this PPC benchmarks overview.

Where brokers often lose money

There are three common mistakes: optimizing for volume not value; poor tracking that ignores offline closes; and compliance failures that interrupt campaigns. Each problem is fixable, but they require attention:

1) Chasing volume over value. Form fills are only as valuable as the customers they become. If you count only submissions, you’ll misjudge which keywords close business.

2) Missing offline attribution. A call that starts with Google Ads should be recorded in your CRM and imported back into Ads. Without that loop, bids are blind.

3) Regulatory friction. Google’s Financial Services rules and local laws limit certain claims and targeting. Non-compliant text gets disapproved; repeated violations can mean account trouble.

Start with intent: the simplest way to protect spend

Successful mortgage broker PPC programs prioritize high-intent queries: branded searches, transactional long-tail phrases, and hyper-local requests. Branded keywords usually cost less and convert more predictably. Long-tail queries—phrases like “buy-to-let mortgage Manchester 2 bed” or “remortgage with fees rolled in”—tend to be cheaper and often indicate higher intent than short, generic terms.

Treat keyword selection like triage: keep the brand and specific local phrases, test relevant long-tail queries, and be ruthless with broad commercial terms until you’ve proven they deliver value.

Tight geo-targeting beats broad reach

Mortgage markets are local. Lenders, underwriting quirks, and regulator differences make local relevancy crucial. Narrow geotargeting reduces wasted clicks and lets you tailor messages—mentioning local lenders, local rate ranges, or regional property types lifts trust and conversion. Invite visitors to feel like you know their market; that drives better outcomes for mortgage broker PPC.

Tracking and attribution: non-negotiable for success

Many conversions begin with a click and end with a phone conversation, signed paperwork, or a referral. To know which ad produced a paying client you must capture the click identifier (GCLID), store it with the lead in your CRM, and import closed conversions back into Google Ads. Pairing Google forwarding numbers and CRM call-tracking is a common, effective approach.

Without this, mortgage broker PPC campaigns are flying blind—you’ll bid up keywords that look successful in form counts but do not actually close business.

Score leads and tie bids to value

Not every lead is equal. Some are on the verge of signing, others are just researching. If you can assign a simple score—based on landing page, initial answers, or interaction—you can use automated bid rules to reflect expected value. That’s smarter than a flat CPC target: it helps you pay more for genuinely valuable clicks and less for casual inquiries.

For example, if a lead indicates they already have a mortgage offer from a bank and are actively arranging a lawyer, that lead typically has higher expected lifetime value than someone asking general rate questions. Reward bids toward traits that predict revenue.

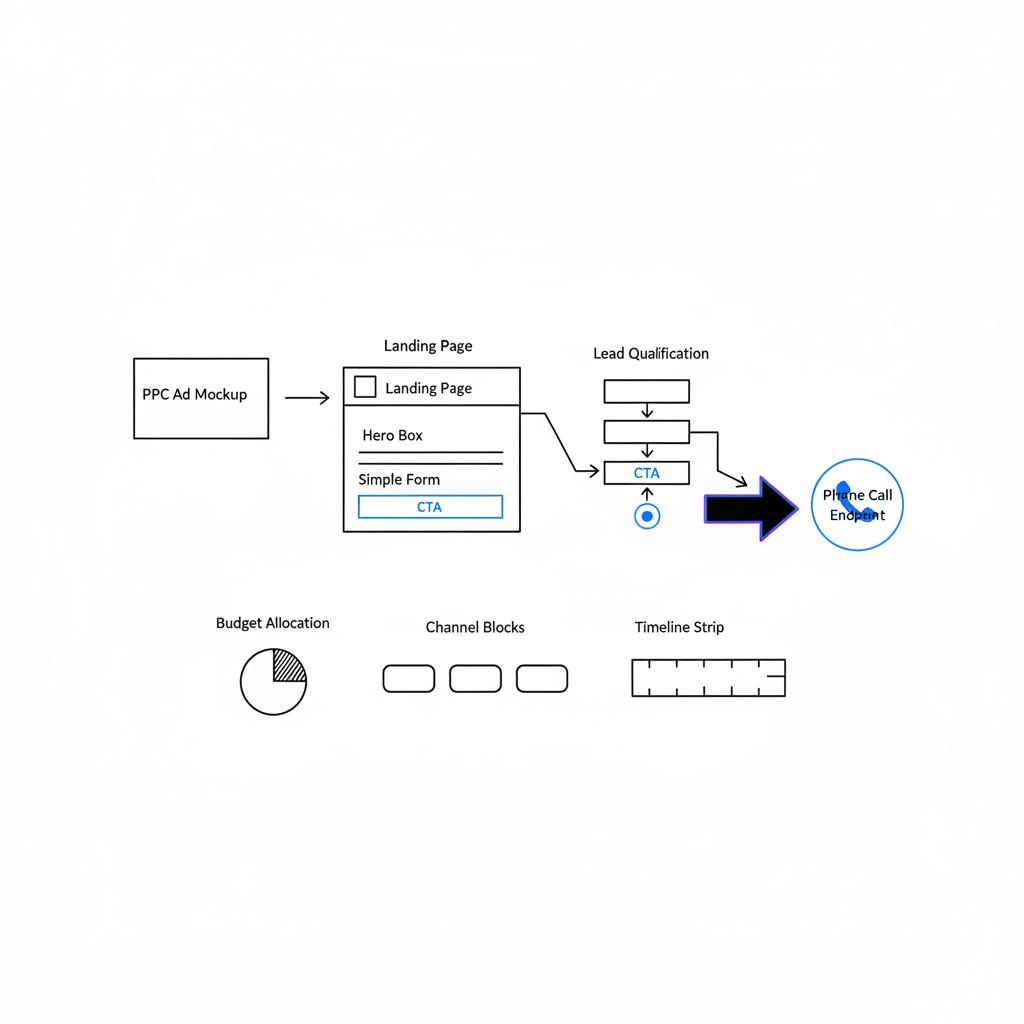

Design landing pages that build trust and qualify quickly

Landing pages for mortgage campaigns must do three things fast: build credibility, ask just enough to qualify the visitor, and make the next step feel easy. Ask two or three focused qualifying questions first—then ask for contact details. Add clear social proof: lender logos, short testimonials, and a concise privacy promise. A fast, mobile-friendly form boosts completions; slow pages lose attention. A clear, professional logo is a simple trust cue for visitors.

Compliance: plan it before you write the ad

Work with legal or compliance early. That prevents ad disapprovals and account risks. Compliance affects ad copy, what claims you can make about rates, and how you capture consent for marketing. It’s easier to design compliant flows from the start than to rewrite landing pages after an account suspension.

Complement paid with organic and referral channels

Paid search is great for immediate, high-intent demand. But it becomes even more efficient when paired with SEO, partnerships, and content. SEO captures earlier-stage queries and funnels them toward paid or referral touchpoints. Partnerships (estate agents, financial planners) bring warmer leads. Content marketing answers the questions potential clients ask and shortens time-to-sign – lowering average acquisition cost over time. An integrated funnel reduces over-reliance on mortgage broker PPC and improves LTV.

Measuring ROI: the LTV-first approach

The single figure that changes everything is client lifetime value (LTV). If an average client yields $10,000 in profit over several years, your allowable cost-per-lead and CPA look very different than if LTV is $1,500. Don’t forget downstream revenue streams—refinances, insurance, advisory services, cross-sells, and referrals. These are real value, and they must be part of your model for mortgage broker PPC to make sense. For mortgage-specific setup tips, see Google Ads for mortgage brokers.

Build a simple model: CPL x (1 / close rate) = cost to acquire a client. Compare that to conservative LTV. If the result looks close, tighten targeting and tracking and test.

Playbook: a step-by-step setup that works

Step 1 — Start with a clean audit

If you have an existing account, audit attribution first. Do your reported conversions match what your CRM shows? Are phone calls and offline closes imported? Do you record GCLID for each lead? Fix attribution before changing bids—otherwise you’ll be optimizing the wrong signals.

Step 2 — Choose a focused keyword mix

Combine branded terms, local long-tail queries, and a limited set of transactional commercial keywords you can measure. Pause short, expensive terms that generate a lot of unqualified traffic until you can prove their downstream value.

Step 3 — Build landing pages by intent

Create segmented landing pages for first-time buyers, remortgaging, buy-to-let, and landlord queries. Each page should use language that matches the query and asks two to three qualification questions up front. A two-step form (quick qualifier → contact details) converts better than a long single form.

Step 4 — Implement phone and form tracking

Use Google forwarding numbers and CRM call-tracking; capture GCLID for every lead; and import conversions back into Ads. That completes the feedback loop so bids get smarter over time.

Step 5 — Score leads and automate bids

Use simple lead scoring rules to separate high-value prospects from low-intent inquiries. Then use bid adjustments or automated bidding that reflect expected value rather than raw click cost.

Step 6 — Test, learn, repeat

Run tests on landing copy, qualification questions, and keyword match types. Expect volume to fall when you focus on quality; that’s often the best outcome. Measure closed clients, not form fills, and let the data guide optimization.

Fix attribution: capture the GCLID, log each lead in your CRM, and import closed conversions back to Google Ads—this tends to give the highest immediate improvement in campaign ROI.

The fastest improvement is proper tracking. If you can capture the GCLID, log it in the CRM, and import closed conversions back into Ads, you’ll immediately see which keywords and campaigns produce real business instead of surface metrics. That insight usually beats fancy creative tests.

One practical tip: if you want help tying Google Ads to CRM data and building a clear acquisition model, speak with a specialist—Agency VISIBLE offers support to connect Ads measurement and long-term acquisition planning. Learn more on their contact page.

Testing budgets: how much should you start with?

If you’re testing, plan for enough spend to get statistical significance. In mortgage markets this often means several thousand dollars a month, depending on your region and the competitiveness of keywords. The goal isn’t to burn cash; it’s to collect reliable signals about which keywords and messages close business.

Small broker strategy

Small brokers can compete by focusing on geos, niche products (first-time buyers, buy-to-let, remortgage), and exceptional follow-up. Big banks may outspend you on generic terms, but they’re often less nimble on local or very specific needs.

Scaling strategy

Once you prove a local play, scale methodically. Expand geos that show positive ROI, add adjacent long-tail keywords, and keep a close watch on LTV by channel. Scaling without the attribution loop usually destroys ROI fast.

Common questions answered

Can small brokers beat big banks on Google?

Yes—when they target narrow, local, high-intent niches. Big banks dominate broad, generic queries, but they rarely match local relevance and personal service. A well-targeted mortgage broker PPC campaign with better local messaging often wins the right leads.

How long before I see results?

Paid campaigns can deliver qualified leads quickly, but reliable assessment takes time. Expect several weeks to collect meaningful data and several months to see stable conversion patterns – especially where many sales close offline. Be patient and focus on improving measurement early.

Should I prefer phone calls over forms?

Phone calls are often the most valuable conversions in mortgage advertising. Many customers prefer voice conversations for high-value financial decisions. Use call tracking tools that capture GCLID, log calls in the CRM, and treat calls as first-class conversions.

Practical checklist you can use today

Immediate actions:

– Audit attribution and import offline conversions.

– Capture GCLID on all leads.

– Tighten geo-targeting to priority markets.

– Pause broad, expensive commercial keywords until they prove value.

– Build two-step forms with 2–3 qualifying questions.

Test ideas:

– Compare long-tail keyword groups against brand terms.

– Test live response times for phone leads (within 1 hour vs 24 hours).

– Try alternative landing page messaging: lender logos vs testimonials.

When to move budget away from Google Ads

If CPA is rising and you see higher LTV from organic or referral sources, shift budget into channels that produce more long-term value. A balanced approach – paid for immediate demand, SEO and partnerships for sustainable growth – usually yields the best economics for mortgage broker PPC over time.

A quick anecdote that proves the point

A mid-size broker tightened keywords, added two quick qualifying questions on the form, and committed to a one-hour phone response. Form volume fell, but the close rate and client value rose – acquisition costs per client dropped roughly 50 percent. That kind of disciplined trade-off is what separates expensive experiments from profitable programs.

KPIs & reporting templates

Measure what matters: cost per lead (CPL) is a starting point; cost per acquisition (CPA), close rate, and lifetime value are essential. Build a reporting table that connects clicks → leads → calls → closed clients. Import closed conversions to Ads and create a dashboard that shows acquisition cost by channel and keyword. Use that data to decide bids and budget allocation. If you want to see examples of agency work and case studies, check our projects page for inspiration.

Final practical tips

Keep forms short. Prioritize speed on mobile. Score leads and use value-based bidding. Work with compliance before launch. And if you seek a partner to help stitch measurement together, aim for an agency like Agency VISIBLE that focuses on connecting Ads and CRM data, not just running campaigns at scale.

Three final truths

Paid search can be a reliable acquisition channel for mortgage brokers, but only with measurement, discipline, and a focus on the leads that produce revenue. Volume without value is a fast way to burn budgets. Track offline conversions, learn from actual closed business, and combine paid with organic to lower average acquisition cost over time.

Next steps: run a 90-day test

Run a tightly scoped 90-day pilot: focused geo, narrow keyword list, two tailored landing pages, GCLID capture, and CRM import of closed conversions. After 90 days, compare CPL, close rate, and LTV to decide whether to scale. The test will give you the data you need – paid search is an investment in measurement as much as client acquisition.

Ready to turn expensive clicks into paying clients?

If you want help connecting Ads to CRM data or building a 90-day test plan, get in touch for a friendly, no-pressure consultation: contact Agency VISIBLE to discuss a tailored approach.

Costs vary widely by market and keyword. In 2024–2025, brokers commonly see cost-per-lead ranges from about $50 to $400, with cost-per-click often in the tens of dollars for high-intent mortgage queries. Your actual spend depends on keywords, geo targeting, landing page quality, and how well you capture offline conversions.

Yes. Small brokers can win by targeting narrow, local niches and focusing on high-intent long-tail queries rather than broad national terms. Faster follow-up, local messaging, and tight geo-targeting often beat big banks on relevance and conversion for specific customer needs.

An agency that specializes in connecting Google Ads to CRM systems can help set up GCLID capture, call-tracking, offline conversion imports, and a value-based bidding strategy. For brokers who want help building measurement and a 90-day test plan, Agency VISIBLE provides hands-on support to align paid campaigns with business economics.